Feeling Crushed by Debt? Take Control with Smart Prioritization

The air in the room grows thin, doesn’t it? Each unopened envelope feels like a ticking clock, each phone call a potential ambush. That crushing weight on your chest, the one that whispers you’re failing, that’s the voice of debt trying to colonize your spirit. But here’s a truth more potent than any creditor’s demand: you are stronger than this invisible enemy. You possess the power to face it, dismantle it, and reclaim your life. Knowing how to prioritize debts when funds are limited isn’t just financial know-how; it’s the first defiant step toward breathing freely again.

It’s about transforming that gnawing anxiety into focused action, that feeling of drowning into the fierce strokes of a survivor swimming for shore. The path isn’t paved with gold, and anyone who tells you otherwise is selling something you can’t afford. But it is paved with something far more valuable: your own resilience.

Your Battle Plan: A Glimpse of the Ascent

When the financial storm rages and resources are scarce, a clear map is your lifeline. This isn’t about magic wands; it’s about strategic warfare. First, you’ll confront the beast: itemize every single debt. Then, you’ll choose your weapon – perhaps the psychological rush of the debt snowball or the cold, hard math of the debt avalanche. We’ll spotlight the absolute non-negotiables, those debts that demand immediate attention, like tax obligations and accounts screaming from collections. A solid budget becomes your shield and sword, and we’ll explore how consolidation or negotiating rates might just be the reinforcements you need. Crucially, you’ll learn to communicate with creditors, not as a victim, but as an architect of your own comeback. And yes, we’ll arm you with knowledge of your rights, because in this fight, knowledge isn’t just power—it’s armor.

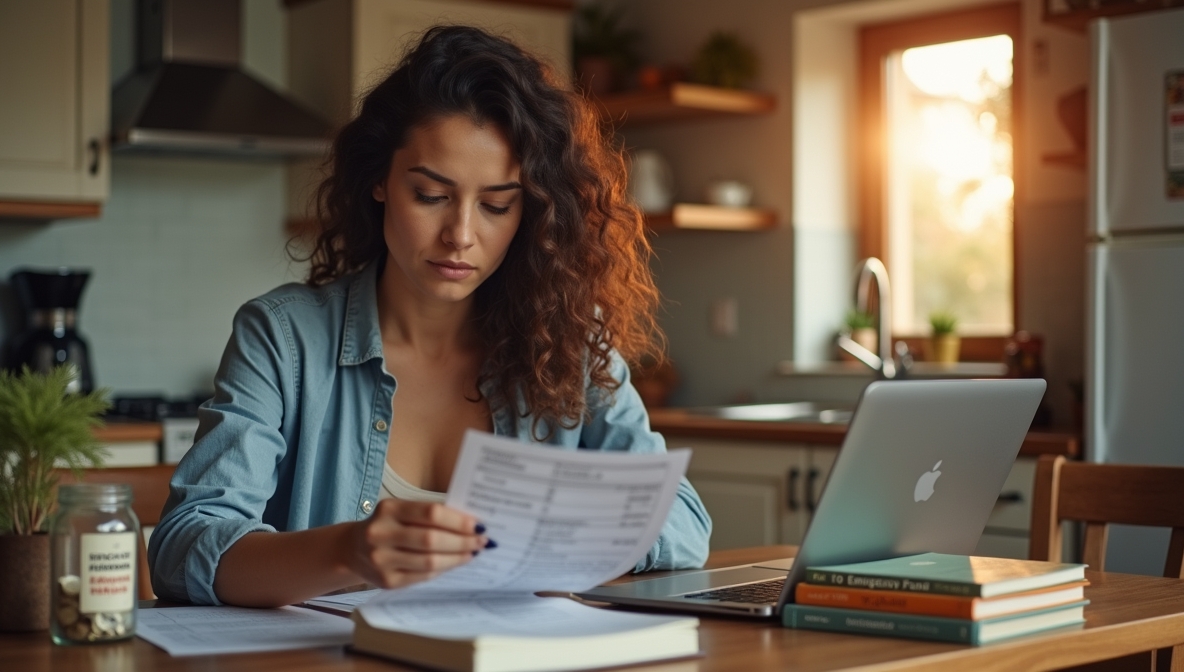

Illuminating the Abyss: Your First Step to Debt Freedom

The fluorescent lights of the late-night diner hummed, casting a sickly pale glow on Amara’s third cup of coffee. Outside, rain lashed the windows, mimicking the storm inside her. A single mother, she juggled food delivery gigs, her car a temperamental beast that devoured what little profit she made. The stack of bills on her passenger seat felt like a physical weight pressing down on the accelerator of her anxiety. Tonight, it was the payday loan, its interest rate a monstrous, many-tentacled thing, that had its hooks in her. Sleep was a distant memory, replaced by calculations that never added up.

Before you can fight, you must know the enemy. Not just its name, but its size, its teeth, its every vulnerability. This means a stark, unflinching inventory of what you owe. Gather every statement, every demand letter, every whispered threat from a collection agency. List them out: who you owe, how much, the interest rate, the minimum payment. It’s an act of courage, like turning on the lights in a monster-filled room. The monsters might still be there, but now, at least, you can see them clearly. And seeing them is the first step to vanquishing them.

This isn’t just about numbers on a page. It’s about acknowledging the reality, however grim, and in that acknowledgment, finding the first flicker of control. That spreadsheet, or even a scribbled list on a notepad, becomes your command center. From here, all strategies flow.

Choosing Your Weapon: The Debt Snowball vs. Debt Avalanche Methods

Once the battlefield is mapped, you need a strategy of attack. Two primary schools of thought dominate the landscape: the Debt Snowball and the Debt Avalanche. Think of them as different martial arts, each with its own strengths.

The Debt Snowball is the emotional warrior’s choice. You line up your debts from smallest balance to largest, irrespective of interest rates. You make minimum payments on all but the smallest, throwing every spare cent at that one until it’s obliterated. Then, you take the money you were paying on that first debt (plus its minimum payment) and roll it onto the next smallest. The psychological victory of quickly eliminating a debt can be incredibly motivating, like a series of small wins that build momentum for the bigger battles. For those who feel overwhelmed, this can be the spark that ignites the fire of persistence.

The Debt Avalanche, on the other hand, is the logician’s preferred tactic. Here, you list your debts by interest rate, from highest to lowest. You make minimum payments on all but the one with the highest, most voracious interest rate, attacking it with everything you’ve got. Mathematically, this method saves you the most money in interest over time. It might take longer to feel that first “win,” but the long-term financial benefit is undeniable. It’s a colder, more calculated approach, but for some, the numbers speak louder than emotional boosts. Which is right for you? That depends on your personality, your financial picture, and what keeps you in the fight. There’s no shame in choosing the path that keeps your boots on the ground and your eyes on the prize.

Red Alert! Debts That Demand Your Undivided Attention

Matt stared at the official-looking envelope from the IRS, the paper feeling brittle and cold in his calloused hands. For thirty years, his hands had expertly guided steel in a now-shuttered auto parts plant. He’d always paid his way, prided himself on it. But since the layoff, navigating the labyrinth of medical bills for his wife, Marisol, and the menacing creep of credit card interest had left him feeling like a stranger in his own life. This tax notice, however, felt different. More implacable. More…final.

Some debts aren’t just annoying; they’re actively dangerous. These are your “red alert” priorities. Topping this list is usually tax debt. The government possesses collection powers that make private creditors look like kittens. They can garnish wages, seize assets, and levy bank accounts with alarming efficiency. Ignoring them is like playing chicken with a freight train. You won’t win.

Similarly, debts that have gone to collections, especially if they’re threatening legal action like lawsuits or wage garnishment, jump to the front of the line. These aren’t just numbers anymore; they’re an active threat to your financial stability and sometimes even your home or livelihood. Secured debts, like mortgages or car loans where the asset itself is collateral, also carry significant weight. Losing your home or transportation because you prioritized a store credit card is a special kind of financial hell. Address these high-consequence debts with fierce urgency before they dictate terms you can’t possibly meet.

Visualizing Victory: An Expert’s Take on Demolishing Debt

Sometimes, hearing it straight from someone who navigates these treacherous waters daily can illuminate the path forward. This video breaks down, with chilling clarity and empowering insight, some of the fastest routes to liberating yourself from debt’s grip. Consider it a masterclass from the front lines.

Video Source: Gabrielle Talks Money on YouTube

The Humble Budget: Your Unsung Hero in the Debt War

A budget. The word itself can evoke images of deprivation, of joyless penny-pinching. But that’s a gross mischaracterization. A budget isn’t a cage; it’s a blueprint for freedom. It’s the tool that shows you where your money is actually going, as opposed to where you think it’s going. And trust me, there’s often a Grand Canyon-sized difference between the two.

Crafting a budget when you’re trying to slay dragons of debt is like sharpening your sword and polishing your shield. It gives you clarity and control. You track every dollar coming in and every dollar going out. This isn’t just about finding spare change for debt payments; it’s about understanding your financial DNA. You might discover a subscription to a cheese-of-the-month club you forgot you had, or that your “occasional” takeout habit is single-handedly funding a small nation’s GDP. These revelations aren’t cause for shame; they are opportunities. Every dollar “found” is another soldier in your army against debt. Creating a budget to pay off debt effectively is the cornerstone of any successful plan for debt management for financial freedom.

Forging a Smoother Path: Consolidation and Negotiation Tactics

Priya meticulously entered numbers into a shared spreadsheet, Mateo leaning over her shoulder, the scent of garlic and onions still clinging to his chef’s whites. They’d merged their lives, their dreams, and, unfortunately, their rather enthusiastic collection of credit card balances from their younger, wilder days. The sheer number of minimum payments, each with its own due date and interest rate, felt like death by a thousand paper cuts. “There has to be a less chaotic way,” Mateo had sighed last week, and Priya, ever the pragmatist, had started researching.

Juggling multiple high-interest debts can feel like trying to herd cats during an earthquake. This is where strategies like debt consolidation can offer a lifeline. The benefits of debt consolidation loans can include simplifying your payments into one, often with a lower overall interest rate. This can free up cash flow and make the repayment journey more manageable. However, approach with caution: ensure the new loan truly offers better terms and that you address the spending habits that led to the debt in the first place. Otherwise, it’s just kicking the can down a more expensive road.

Another powerful, often underutilized, tactic is direct negotiation. Did you know you might be able to negotiate lower interest rates on credit cards simply by asking? Many people don’t realize that creditors are often willing to work with borrowers who are genuinely trying to meet their obligations. A polite, firm phone call explaining your situation and requesting a rate reduction costs you nothing but a little time and courage. The worst they can say is no. The best? You save a significant amount on interest, accelerating your journey out of the red.

Beyond the Balance Sheet: The Human Element of Debt

The silence on the other end of the phone was heavy, a pregnant pause that made DeShawn’s palm sweat. He was calling his credit card company, the one with the interest rate that seemed to mock him with its monthly climb. He’d rehearsed what he wanted to say – about the unexpected medical bills, the reduced hours at his warehouse job. He wasn’t asking for a handout, just a lifeline, a temporary reduction in his payment, maybe even that interest rate. The fear of judgment, of a cold, corporate “no,” was almost paralyzing.

Creditors are not faceless monsters (mostly). They are businesses, and often, it’s in their best interest to work with you rather than write off a debt entirely. Communication is key. If you’re struggling, don’t bury your head in the sand like a financially ostrich-ized… well, ostrich. Reach out before you miss payments. Explain your situation honestly. They might offer forbearance, a modified payment plan, or other hardship options. This proactive approach can prevent accounts from going to collections and damaging your credit further.

And if the sheer weight of it all feels too much, if navigating the system feels like trying to decipher ancient hieroglyphics while blindfolded, consider professional help. The role of credit counseling in debt management can be invaluable. Reputable non-profit credit counseling agencies can help you create a budget, negotiate with creditors on your behalf, and develop a Debt Management Plan (DMP). They aren’t miracle workers, but they can be powerful allies, providing structure and expertise when you feel lost in the fog. Just ensure they’re accredited and not some predator disguised as a savior.

Know Your Shield: Rights and Realities in the Debt Arena

The letters started arriving daily, each one more aggressive than the last. A debt collector, for a medical bill Consuela was sure had been covered by her previous employer’s insurance, was employing tactics that felt less like collection and more like harassment. Early morning calls, threats of legal action she didn’t quite understand, even a call to her neighbor. The stress was a constant thrum beneath the surface of her days as a home health aide, making it hard to focus on her patients.

When debt collectors come knocking, or rather, incessantly calling, it’s crucial to know you have rights. The Fair Debt Collection Practices Act (FDCPA) is your federal shield against abusive, deceptive, and unfair debt collection practices. Collectors cannot harass you, lie to you, or use unfair tactics. They can’t call you at unreasonable hours, contact you at work if you tell them not to, or discuss your debt with third parties (with some exceptions). Knowing this can empower you to push back against bullying tactics. Document everything. Send cease and desist letters if necessary.

Sometimes, the mountain of debt seems so insurmountable that debt settlement appears like an oasis in the desert. This involves negotiating with creditors to pay a lump sum that’s less than the full amount owed. While it can provide relief, it’s critical to understand the legal implications of debt settlement. Settled debt can be reported as “settled for less than the full amount” on your credit report, which can negatively impact your score. Additionally, the forgiven portion of the debt may be considered taxable income by the IRS. It’s a complex path, often best navigated with professional advice, lest your escape route lead to a different kind of trap.

Avoiding the Quicksand: Common Mistakes and Credit Score Realities

It’s easy to stumble when you’re navigating a minefield. One common pitfall is the ostrich approach – ignoring the problem, hoping it will magically disappear. Spoiler: it won’t. It festers. It grows. It eventually explodes. Another is falling for “too good to be true” debt relief scams that promise to wipe your slate clean for a hefty upfront fee, then vanish like smoke. Always research any company offering debt help.

Many also make the mistake of draining essential retirement savings to pay off unsecured debt. While the desire to be debt-free is understandable, compromising your future security can be a catastrophic error. Understanding how to avoid common debt management mistakes is as vital as knowing which debts to pay first. Similarly, be acutely aware of the impact of debt settlement on credit score; while it might solve an immediate crisis, it can leave a long shadow on your creditworthiness, making future borrowing (for a home, a car) more difficult and expensive.

The journey of learning how to build wealth with a low income often begins with mastering debt. Each misstep avoided is a step closer to stability.

Arming Yourself: Your Debt Management Toolkit

You’re not alone in this fight, and thankfully, technology and resources have evolved to offer some nifty backup. Think of these as the gadgets in your utility belt:

- Budgeting Apps: Tools like YNAB (You Need A Budget), Mint, or Personal Capital can automate tracking your spending, categorizing expenses, and visualizing your cash flow. They force an often-uncomfortable intimacy with your financial habits, which, frankly, most of us could use.

- Debt Payoff Calculators: Search online for “debt payoff calculator” and you’ll find a plethora of free tools. These can help you visualize how different payment strategies (like snowball vs. avalanche) impact your payoff timeline and total interest paid. They turn abstract numbers into concrete projections, which can be incredibly motivating – or a much-needed kick in the pants.

- Spreadsheet Software: Good old Google Sheets or Microsoft Excel. Sometimes, the most powerful tool is the one you customize yourself. Create your debt inventory, track payments, project interest – become the master of your own financial data. It’s less flashy, perhaps, but deeply empowering.

- Credit Monitoring Services: Companies like Credit Karma or Experian (often free versions are available) allow you to keep an eye on your credit report and score. Knowing where you stand helps you track progress and spot any inaccuracies or fraudulent activity, because Murphy’s Law dictates that when you’re already down, someone will try to kick you.

The best tool is the one you’ll actually use consistently. So experiment, find what clicks, and integrate it into your financial life. It’s about making the overwhelming manageable, one small, organized step at a time.

Navigating the Fog: Your Debt Prioritization Questions Answered

When you’re wrestling with the question of how to prioritize debts when funds are limited, confusion can be your worst enemy. Clarity is your ally. Here are some common queries from the front lines:

What if I truly can’t afford even the minimum payments on all my debts?

This is a red-flag crisis moment. Your absolute essentials – shelter (rent/mortgage), utilities to keep that shelter habitable, food, and critical medications – come first. After that, prioritize secured debts where you could lose an essential asset (like your primary car if you need it for work). Then, high-priority debts like taxes or child support. For the rest, you may need to proactively contact creditors to explain your situation and negotiate forbearance or a temporary hardship plan. This is also a prime time to consult a non-profit credit counselor. Ignoring it is not an option; it will only escalate.

Is it ever okay to prioritize low-interest debt if it causes me more stress?

This is where the “personal” in personal finance really shines. Mathematically, attacking high-interest debt first (the avalanche method) saves you more money. However, if a smaller, low-interest medical bill is keeping you up at night due to aggressive collection tactics or a deep-seated emotional trigger from a past experience – say, with a particularly unsympathetic billing department – then paying it off for peace of mind can be a valid choice, provided it doesn’t severely derail your progress on much larger, more dangerous high-interest debts. Amara, our delivery driver, might find eliminating a small, nagging utility bill gives her the mental bandwidth to tackle the payday loan shark with renewed vigor. It’s a balance. The key is to make a conscious, strategic choice, not an impulsive one.

How does prioritizing debt repayment affect my ability to save for an emergency or for the future?

It’s a tightrope walk, no doubt. Most experts recommend establishing a small emergency fund (perhaps $500 – $1,000) before aggressively tackling debt. Why? Because life happens. The car breaks down, the kid gets sick. Without that small buffer, an unexpected expense can force you to take on new debt, undoing your hard work. Once that mini-emergency fund is in place, you can throw more resources at high-interest debt. Long-term savings, like for retirement, are crucial. If your employer offers a 401(k) match, try to contribute enough to get the full match – it’s free money. Beyond that, the balance shifts depending on your debt’s interest rates. High-interest credit card debt (20%+) often takes precedence over investing returns, as your “guaranteed return” by paying it off is that high interest rate you’re no longer paying. Low-interest debt (e.g., a 3% mortgage) might allow for more aggressive saving/investing simultaneously. Matt, the former machinist, might pause extra payments on his low-interest mortgage to rebuild his emergency fund once the threatening IRS issue is resolved.

What if a debt is really old? Do I still have to pay it?

Debts have a statute of limitations, which is a legal time limit for how long a creditor or collector can sue you to collect. This varies by state and by type of debt. If a debt is past the statute of limitations, you may no longer be legally obligated to pay it (though it might still appear on your credit report). However, be very careful. Making a payment or even acknowledging the debt in writing can sometimes restart the clock on the statute of limitations. If you suspect a debt is very old, it’s often wise to consult with a legal aid service or consumer protection attorney before engaging with the collector. Don’t just take the collector’s word for it; they have a vested interest in, shall we say, creative interpretations of timelines.

Beyond the Horizon: Charting Your Next Steps

The journey to financial well-being is ongoing. Arm yourself with more knowledge:

- Equifax on Prioritizing Debt Payments: Solid insights from a major credit bureau.

- FTC on Debt Collection FAQs: Know your rights under the FDCPA.

- National Foundation for Credit Counseling (NFCC): Find accredited non-profit credit counselors.

- Money Fit on Handling Credit Card Debt: Specific advice for a common struggle.

- r/personalfinance: A large community discussing all things money, including debt.

- r/debtfree: Stories, support, and strategies from people on the same path.

- Prosper Blog: What Debt to Pay Off First: More perspectives on prioritization.

Ignite Your Dawn: The First Step is Yours to Take

The weight is still there, perhaps. The path ahead still looks steep. But now, you hold a map, a compass, and the undeniable truth of your own capacity to change your stars. Learning how to prioritize debts when funds are limited isn’t just an intellectual exercise; it’s a declaration of war against despair, a promise you make to your future self. That future self deserves peace, freedom, and the quiet joy of financial stability.

Don’t wait for the “right moment.” The right moment is forged in the fire of decision. Pick one thing from this guide – just one – and do it. Today. Make the list. Call one creditor. Research one budgeting app. That single act, however small it feels, is the spark. Fan it. Feed it. Let it grow into a wildfire of resolve that consumes your debt and illuminates your path to a life unburdened. Your ascent starts now.